India is sitting on a growing pool of money that no one is using, not because it is not needed, but because it has slipped out of sight. Unclaimed assets across bank deposits, shares, insurance policies and retirement funds are estimated at Rs 2.2 lakh crore, according to a new 1 Finance Magazine study.

What is more concerning is that this figure has grown sharply over the past five years, highlighting gaps in succession planning, documentation and financial awareness.

In most cases, the money has not vanished. It sits in accounts that stopped moving, investments that were never tracked again, and claims that were never filed.

Over time, the link between the asset and its owner weakens, and eventually breaks.

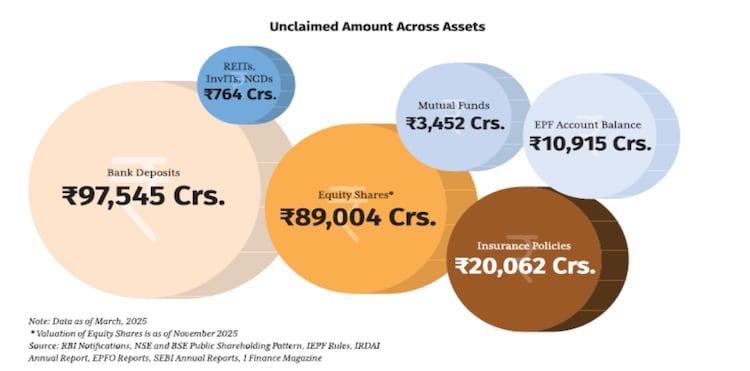

The largest share lies in bank deposits. Nearly Rs 97,545 crore has accumulated in the Reserve Bank of India’s Depositor Education and Awareness Fund, growing at 24% annually. Dormant accounts are steadily transferred into this pool, where the money remains but becomes harder to trace.

Much of this comes from an earlier era of finance, when accounts were opened with physical records and rarely consolidated.

Once a bank account stays inactive for 10 years, the money is moved by the bank to a fund managed by the Reserve Bank of India. The money does not disappear. It can still be claimed at any time by the account holder or their family through the bank, which then settles the claim with the RBI.

Until that happens, the money earns a low fixed return, currently around 3%, and is used for depositor awareness programmes.

The ownership stays with the depositor, but the money is no longer held directly with the bank.

A similar pattern is visible in the equity markets. Shares worth Rs 89,004 crore, spread across 166 crore shares in 1,671 companies, have moved to the Investor Education and Protection Fund Authority after remaining unclaimed.

If dividends remain unclaimed for seven years, both the dividend and the underlying shares are transferred to the IEPF, where they remain until claimed.

Some of these holdings date back decades, continuing to gain value while their owners or heirs lose track of them. A significant portion is concentrated in a handful of companies, including Reliance Industries.

Insurance policies account for Rs 20,062 crore in unclaimed maturity proceeds, death benefits and surrendered policies.

Unclaimed insurance proceeds stay with insurers for up to 10 years before being transferred to a government fund, where returns no longer flow back to policyholders.

Retirement savings show the same drift. Rs 10,915 crore is locked in 31.87 lakh inoperative EPF accounts, many of them untouched for years. Nearly 38% of these accounts have been inactive for 5 to 10 years, and 21% for more than 20 years.

EPF accounts are classified as inoperative after three years of inactivity, often due to job changes or lack of tracking across employers.

Newer financial products are now adding to the pile. Mutual funds account for Rs 3,452 crore in unclaimed dividends and redemptions, while REITs, InvITs and similar instruments contribute another Rs 764 crore, growing at over 31% annually.

Unclaimed payouts are parked separately and remain claimable, but any gains after a certain period may no longer accrue to the investor.

WHAT HAPPENS TO UNCLAIMED ASSETS?

The pattern cuts across the system. As more people enter formal finance and spread their money across multiple products, the chances of losing track of some part of it increase. What happens to this money once it slips out of reach is less visible.

The legal right to claim it remains with depositors, investors and their families. But the benefits generated along the way do not always flow back.

Simply put, ownership of assets stays, but value and access drift away over time.

Animesh Hardia, Editor-in-chief of 1 Finance Magazine, told me the benefits of this money rarely reach its rightful owners. “The government’s funds and institutions hold this money, not the families it belongs to. Each asset class parks unclaimed money differently, but in every case, the owner or their heir loses value over time.”

Bank deposits in the DEA Fund, he pointed out, earn only 3% simple interest, lower than inflation. That fund is used for depositor education and awareness.

Shares transferred to the IEPF remain market-linked, but corporate benefits earned during that period do not go back to the claimant. Insurance money stays with insurers for years, where it is invested and partially retained before eventually moving into government-managed funds.

“The legal right to claim exists,” Hardia said. “But the actual money, the returns, the compounding, the income goes elsewhere with each passing year.”

WHY FINDING YOUR OWN MONEY IS SO HARD

That disconnect is reinforced by how the system itself is structured. With different asset classes governed by different regulators, there is no single way to track what an individual owns.

Abhishek Kumar, a Sebi-Registered Investment Adviser (RIA) and founder of Sahaj Money, told me that fragmentation sits at the centre of the problem.

“The problem has multiple facets with fragmentation as the primary roadblock. As many of these asset classes are regulated by separate regulators, hence a unified cross-institutional registry for tracking holdings is missing for most of them,” Kumar said.

“The system breaks down most often during life events such as address changes or the death of an account holder, where outdated KYC data prevents financial institutions from successfully reaching the rightful owners or heirs,” he added.

This is unfolding alongside rapid financial digitisation. Opening accounts and investing has become easier. Tracking money across a lifetime has not. Each asset class operates within its own system, with separate records and processes.

There is no single view of an individual’s financial holdings.

The gaps become visible when families try to recover money. Financial information is often scattered. Nomination details are missing or outdated. Documents are incomplete. Even after identifying assets, reclaiming them can mean dealing with multiple institutions, each with its own requirements.

The study highlights three persistent gaps: poor nomination practices, low awareness of recovery mechanisms, and fragmented reclaim processes.

Hardia sees the problem as both behavioural and systemic, but with different degrees of difficulty.

“The household failure is simple. People invest but do not document, do not update nominees, and do not tell their families,” he said. “The system failure is that there is no one place for a family to check what they own across banks, insurers, EPFO and mutual funds.”

Kumar pointed to the same gap from a different angle. “Digital portals have improved access, but they cannot solve the problem of families not even knowing an account or investment exists,” he said.

THE SILENT EROSION OF HOUSEHOLD WEALTH

There is also a steady erosion in value. Unclaimed bank deposits transferred to regulatory funds earn about 3% simple interest, below inflation.

Over time, purchasing power declines while the money remains unclaimed.

“This is a significant but overlooked erosion of wealth,” Kumar said. “Capital earning below inflation loses real value every day it remains dormant.”

The distribution is uneven. In EPF accounts, almost half of the unclaimed corpus sits in just 0.4% of accounts. At the same time, millions of smaller accounts lie dormant.

What this essentially means is that nearly half of the EPF corpus is concentrated in just 0.4% of accounts.

The system has been built to make investing easier, but not to ensure continuity. Money can be put in quickly. Tracing it later is far more difficult.

LEGAL RIGHT EXISTS, BUT ACCESS IS HARD

The legal framework, however, draws a clearer line. Ownership does not disappear, even when the money moves.

Shabnam Shaikh, Partner at Khaitan & Co, said the status of ownership depends on the nature of the asset, but the underlying rights of the claimant remain intact.

“There is no change in legal title with respect to the deposit account,” she said. “The claimant does not lose the right to the asset. What changes is control, which can be restored once a successful claim is made.”

In the case of bank deposits, funds are transferred to the Depositor Education and Awareness Fund but can be reclaimed through the bank, which then seeks reimbursement.

Shares, however, follow a different route. If dividends remain unclaimed for seven years, both dividends and shares are transferred to the IEPF’s demat account, where they remain linked to a “rightful owner,” with voting rights frozen until they are reclaimed.

“There is no ‘erosion in control’ per se,” Shaikh said. “The claim itself is not extinguished due to any time limit under the extant regulatory frameworks.” She added that the success of a claim often depends on the ability to produce the required documents.

Across asset classes, claims typically require identity proof, account details, nominee records and, in many cases, succession documents, making the process difficult for families, especially when records are incomplete.

WHY UNCLAIMED ASSETS KEEP RISING?

While regulators have put in place notice requirements before such transfers, the system still largely depends on individuals or heirs coming forward. Unclaimed financial assets often arise from gaps in succession planning and poor communication with legal heirs about the existence of assets and documentation.

The scale of unclaimed wealth also reflects deeper gaps in succession planning. In most cases, nominees hold assets on behalf of legal heirs, except in certain cases such as life insurance policies.

“There is a lack of awareness with respect to how the nomination mechanism functions vis a vis testamentary or interstate succession,” Shaikh said. “Most of the times, the heirs or the nominees are unaware of the assets held by a deceased.”

Without clear documentation and communication, the process of transferring wealth becomes fragmented even after death. Tools such as wills, trusts and succession checklists remain underused.

{kind=link}